Palantir - volatility and risk

Two for one deal: value and growth

So yeah, I own PLTR 0.00%↑ . I’m used to volatility through my forays with crypto and TSLA 0.00%↑ . I got in on it in the ‘hype-train’ area of history, just as the US started to reverse it’s decade long QE towards a QT approach so, yeah, I’m deep in the red.

My reasoning was that I’m looking for a stock to place my cash after TSLA’s run-up (and a small fruitful bet on GME 0.00%↑ - thank you /wsb). I’ve heard of this company vaguely from the media though to my knowledge they had no intention of going public. I learned of it’s DPO a few months after it happened and immediately started building a position. Hindsight 20/20, I know. But I’ve been witnessing the american government pumping money in it’s economy during the lockdowns and I’ve thought that this won’t end well so I’ve been looking for a company that can weather a recession, with which I’d have no problem riding it’s ups and downs. Enter Palantir, with it’s self-entitled war-chest of 2,3 billion $ and no debt. This, I thought, is a company that has virtually no risk of going bankrupt.

As it’s valuation went a bit crazy with the whole meme-stock phase I divested a bit towards Romania’s stock market in no small part due to my idea that americans are printing too much money. That ended up being a nice idea.

I’m also a bit of a gambler so if I have idle cash I’ll throw it to side-hustles or stocks - I’ve tried being disciplined, whatever that means, but whenever PLTR went lower, I figured that’s an opportunity to DCA (as I’ve did fairly successfully before with both btc and tsla).

I’m still bullish on the stock, and whenever I get extra cash I just dump it in to the 'dumpster fire’. I’m pretty confident that I’ll end up ahead in 10 years time with my strategy though I guess we never know. After all - bears all say that this is a company that after 20 years it didn’t reach profitability, that it’s paying it’s owners and employees with SBC, that it’s a consulting company disguised as a SaaS… all of which I’ll go into.

I’ve laid out a ToC but before that, a short intro.

So over the past 10 years we’ve went from mySpace to everyone having iPhones with more computing power than the ones available to NASA when humanity supposedly sent people to the moon.

To me, it’s crazy - I’m a fucking pleb in Eastern Europe. I can buy a partial ownership in a CIA backed firm - all from the comfort of my couch with a neat app on my phone.

I’m not the only one. People around the world are playing stocks nowadays. The previous idea of ‘get out when your taxi driver starts talking about a stock’ is, well to some degree still sort of correct but in other areas not. Our global economy is so interconnected it’s crazy. Almost all of my friends and acquaintances have dabbled on the stock and crypto market, going in and out of positions in Apple, Google, whatever. I’m in a country that’s basically qualified as 3rd world.

That’s fucking crazy. Who would have thought 10 years ago that nobodies from East Europe could own parts of companies that drive world-wide innovation? I certainly didn’t. So that’s what in part drives my thesis with palantir as well. As the whole world is looking to chase ROI that means tons of fairly smart, educated people, now have access to the global stock market from their phones. And then there’s us dumb fucks that learned that buy, dca and hold works eventually.

I’m guessing most of us will HODL through the down-turns and not let the greedy hedge-funds get their grubby hands on our precious shares. As of right now, I’m down 70% and averaging down - and will continue to do so even if (and especially if) it reaches it’s prophesied $5 stock - at that point that’d be close to a 10 bln. valuation - which would place it at 4x cash (that’s not considering it’s remaining deal value of $3,5 bln. and money invested in IP, patents and development). That’s nuts. Macro be damned you bet I’ll be going all in on that. Yes, I know, management has controlling shares - I’m just grateful to be able to build a position in a company where some of the most intelligent minds have been dedicating their lives for the past two decades.

So anyway…

1.0 What does the One World Government has to do with PLTR?

2.0 What does Palantir do? Two in one deal: government contractor with a new commercial platform

3.0 Palantir’s strategy of lots of small bets (PLTR for builders, SPACs, dev community, partnerships)

4.0 It’s sales strategy, current and potential valuation, bear case and risks

5.0 It’s raving fan base

6.0 Additional copium & reading material

Let’s get this out of the way…

1.0 What does the One World Government has to do with PLTR?

Well, for starters - both Peter Thiel and Alex Karp are invited to the Bilderberg meeting for over 10 years IIRC. Here’s a link to an article that outright mentioned New World Order and Palantir in the same sentence. Here’s Alex Karps’s own WEF page - of course, he’s also attented the Davos meetings.

So yeah Bilderberg, Club of Rome, Commitee of Foreign Relations… they’re all true. To deny this means either you’re denying reality either you prefer to duck your head in the sand and scream ‘la-la-la-la-la’ when you hear of conspiracy theories.

And when Peter Thiel told us in the reddit AMA close to 8 years ago that PLTR is a front for CIA… I sorta believe him, even though it was a bit of a tongue in cheek reply to a question.

Speaking of the CIA and it’s friends, remember project DARPA LifeLog?

According to its bid solicitation pamphlet in 2003, it was to be "an ontology-based (sub)system that captures, stores, and makes accessible the flow of one person's experience in and interactions with the world in order to support a broad spectrum of associates/assistants and other system capabilities". The objective of the LifeLog concept was "to be able to trace the 'threads' of an individual's life in terms of events, states, and relationships", and it has the ability to "take in all of a subject's experience, from phone numbers dialed and e-mail messages viewed to every breath taken, step made and place gone".

…

Another of DARPA’s goals for LifeLog had a predictive function. It sought to “find meaningful patterns in the timeline, to infer the user’s routines, habits, and relationships with other people, organizations, places, and objects, and to exploit these patterns to ease its task" [2][3]

The LifeLog program was canceled in February 3rd, 2004 (one day before the launching of Facebook), after criticism concerning the privacy implications of the system.

So one day before FB launched, LifeLog got canceled? Surely coincidental.

Who is the first outside investor in FB? Thiel.

Why wouldn’t I invest in Skynet if the guys in charge are rubbing elbows with all the other cool kids? Maybe it’s AI will have mercy on it’s shareholders. I, for one, welcome our new overlords.

2.0 What does Palantir do? Two in one deal: government contractor with a new commercial platform

2.1 Foundry

It’s a platform to help big businesses create a “digital twin” of their business with the goal of making better decisions. It provides competitive advantage in a world where corporations compete in ekeing out tiny margins that mean big $ in volume. Best to watch the videos a couple of times though so you can get how massive this platform really is.

They had a different working product called Metropolis and they scrapped that to launch Foundry in 2019 before it’s DPO. So they basically took Gotham, it’s government oriented platform, which they’ve funded with Uncle Sam’s money, and are now taking it to market. In just 3 years they’ve signed up over 200 new commercial clients.

They say it’s an operating system for the modern company. I think it’s so much more - as it enables new industries that just couldn’t have been possible without Foundry.

In a few words, it has 5 layers:

Data integration from whatever sensors you can imagine (be it valves on a plane, doo-dads on satellites) to excel files and ERP systems.

Search and discovery facilitating single point of access access that allows a user to search in any of the databases across an enterprise. A non-technical analyst can perform advanced conceptual and persistent searches of petabytes of data without using SQL queries or by writing strings. It lets an analyst discover the unknowns by allowing them to search on the basis of how different information is linked together.

Knowledge management and version control - system that can grant different levels of access to different people from within the organization and vendors or partners from it’s supply chain.

Collaboration and version control - individuals and groups of individuals benefit from each other’s work while making sure that each user can access only the data s/he is authorized to access. This way data scientists for example can each work on the same data sets and share relevant insights without losing track of changes. This is so massive that I can’t even.

Machine Learning - so basically once you feed the machine enough data, it learns how errors occur (even without humans being able to accurately understand why) and can display alerts on said errors. With time, it learns even more - up to eventually predicting that there will be an error. Predictive maintenance is all the rage, and enables tons of cost savings for companies.

I’ve gotten the above 4 items from this guy’s study on Palantir's over 1500 patents, to which I've added the ML idea. 1

I think the ML layer is extra juicy for companies. The best explanation of how this works I got from a reddit user: 2

An airline I work for signed up to the 'skywise' platform 2 years ago which is owned by Airbus and powered by Palantir's Foundry software.

The benefit is that all of our previous software could be merged from the backend into one user interface. Things such as aircraft fault codes, sensors data on the aircraft, engine parameters, fault history, internal part inventory, reliability data, aircraft log book data, aircraft delay reports and much much more. Previously all of these data points were using different types of software and language which was not compatible with one another. You'd need a user name and password for each program and it would take forever to get a holistic view of what was happening with the fleet.

1st Phase - Implementing foundry to begin analysis.

Once the data merge was complete we could focus on delay reduction and limiting / preventing aircraft system failures. We began by being able to now get live aircraft data in real time while its 40,000ft in the air and check what is faulting. For example; lets assume Engine 1 bleed air HP ( High pressure ) valve was failing in the open position.

I can now from one single display click on the fault code ( within foundry Skywise ) which will allow me to show any previous faults the aircraft has had with this valve, when were there any pilot reports of this valve faulting on other flights, when was this valve installed on the aircraft, what the history of the valve, when did it come from another aircraft and was it with the same fault years ago? And what was done on the last repair visit for this valve. I also have the ability to see if we have inventory spare parts to replace the valve and if not what other airlines have this item so i can look for a 'loan'. I have the choice now to replace this valve and have engineers ready to do the job before the aircraft even lands on the ground.

This is a great result compared to wait for the plane to land and then the pilot informing engineers that there is a fault and them to have to manually find all of the above information out. But foundry is much much better than this....

2nd Phase - AI - Predicting failures - the real beauty of foundry.

This part is where the cost benefit really shows its true colours. Lets use the HP valve example again only now with foundry data tech reverse engineering faults but looking at when this valve fails with older raw data and then building algorithms and fault thresholds to predict BEFORE a valve is going to fail. I'm going to try make this example as basic as possible but there are so many more parameters used with this valve like throttle command position, bleed air demand, engine EPR etc....

So in basic as terms: The HP valve should open/close within 2.5seconds, if it takes over 3.5seconds it will fault or if it jams in an uncommented position it will also fault. In foundry we've made the algorithm's trip to notify us of an impending fault if the aircraft has 3 occurrences within the last 10 flights where the HP valve close/open rate was between 3sec - 3.45sec. We can then have a graph showing us the last 100 days flights with open / close times where we will see when the valve was new it may have taken 1 second but as it begins to wear the time to open / close gets longer and longer. You see a clear upwards trend in the valve open / close time over months of flying.

From here we can now see that this valve is close to failing and if it did it would either ground the aircraft in a port with no spare parts or cause very significant delays and flight cancellations. What we are doing now is effectively changing this HP valve change from a 'unscheduled' event to a 'planned maintenance visit' Where we can change this valve before there's any disruption to the network and no loss of revenue.

Factor in a cancellation on a flight from New York to Paris on an A380 - Imagine having to put 550 passengers in hotels plus transport for one night while the aircraft is broken and then send a recovery flight to get the stranded passengers from Paris who are waiting on this aircraft to take them home to New York. There's literally hundreds of thousands of dollars being saved on one cancellation, factor in a network of 260 aircraft where your preventing up to 30 cancellations a day, the savings are astronomical.

Further to this benefit of foundry we have also found huge savings in part repair costs. This HP valve is being sent for repair when effectively the aircraft hasn't even see it fault yet. That means the valve is still in good condition and the majority of the time the valve just need a basic bearing and flap change rather than a full overhaul or worse yet a whole new Electric motor & valve. The cost difference in just this alone is close to $20,000 between repair and full overhaul.

There are hundreds of algorithm's we've done to predict a whole range of failures to decreasing tyre pressure limits, brake wear limits, engine vibration, landing gear prox sensor inductance limits etc etc etc, the possibilities seem endless. Its making flying ALOT SAFER for the passenger which is a great thing.

Also, they continually invest in R&D and further develop new offerings. From the most recent Q2/2022 Business Update, they’ve developed the following products and services since the company’s DPO: Edge AI, HyperAuto, Cosmos, MetaConstellation, Appollo for customer’s SaaS, Pipeline Builder, Titan, Nexus Peering, Gaia AI, .

And that’s in addition to the already existing platforms that are built using foundry tailored for particular industries: one for energy and utility companies, one for healthcare providers, one for the aviation industry (Skywise), one for financial services, compliance and fraud, one for the carbon emissions supply chain industry with Transfigura, etc.

2.1 Gotham

So they initially secured funding from US government to build out the platform for a joint database for the FBI and CIA if I recall, after which they’ve expanded their tentacles across the US government and across a few other allied governments.

It’s been selected for a contract with the National Nuclear Security - IMO, like Antonio Linares 3 mentioned, if they’re good enough for them, they’re good enough for me.

Other clients include the DHS, Space Force, Air Force, NSA, USA’s Intelligence Community, DoD (which they’ve successfully sued as crazy as it sounds), the CDC, Marine Corps and likely a few others that they can’t share for security reasons. They’ve hinted at some government partnerships across Europe though.

So how I think of this - it’s a government contractor with a sticky business model, so it’ll be connected directly to USA’s money printer for quite a while. This, to me, means continuity, and safety. That’s a rare aspect for growth stocks.

So if it’s commercial endeavors don’t end up delivering as expected by 2030? I think it’s safe to say they have a solid footing in the US government, so there’d need to be a spectacular event for it to go to 0.

I won’t even go into Apollo, it’s connective tissue software or it’s different offerings as I’m not that smart and this could go on for quite a while. I’ll provide in the last chapter additional links you can check out.

3.0 Palantir’s strategy of lots of small bets (PLTR for builders, SPACs, dev community, partnerships)

3.1. SPAC’s

Lots of burnt folk are bitter about PLTR’s SPAC investments. I’ve even read people argue that the company should return money to it’s shareholders so they can each decide whether to invest or not in risky SPACs (lol). For that lot, please take your money to stable dividend paying companies.

Some people are complaining that this is “buying revenue”. I view that as good business - so they invest straight cash today (which, accounting for the ‘time value of money’ formula, means is more important than future cash) while they offer their platform to new start-ups in up and coming areas that cam further demonstrate Foundry’s adaptability in industries no one would have thought possible even just a few years ago and they get to earn that cash back with a lil extra on top all while learning all sorts of new data to feed the basilisk? AND - they get to keep their position in the company basically for free - no, they’re paid to invest in the company over the course of their contract?

Sure - the marketable securities part of their balance sheet doesn’t look nice. Now. That’s not even the point. Data and proof of concepts are what they’re angling for from a product stand-point - making a 10x on their investment is the cherry on top. I think they’d be ok even if they all go to 0 (unlikely IMO).

Plus, their valuation right now after most of them dropped ¬94% is fairly sensible so if they manage to survive, this may be a promising entry point for the savvy gambler investor. Not to say they can’t go down another 94% though - do your own damn research, you know the drill. The businesses are in their infancy and if you remember Wright’s Law, they might be on to something. Though as US is entering a who-knows-how-long QT era (I myself never have experienced it, as I guess most of us millennials never have), seeing as how most of these SPAC’s were or are pre-revenue, they could go all down the drain. That said, I think if they do end up trading lower, some rich capitalist will swoop in and buy it on pennies on the dollar. Hell, maybe even Palantir ends up buying a whole distressed company - after all, they have inside-info on how it’s going due to their continuing relationship. Some of them do have interesting tech for the future, so even if they end up having to appeal to the capital markets (which are tightening their butt-hole as we speak) and I think it’s a likely probability considering most of them have pretty high burn rates, the appeal is there.

Going beyond that - have you seen all the free press their SPAC strategy this generated? All the cool magazines in business and finance published something about this. That’s incidentally, what most high-flying CEOs read (not reddit like us poors). And extra publicity? We’re in an age where people are likely to change companies every few years. Even if all the SPACs go to 0 - the people working at them will likely continue working in similar industries. Think they’ll be talking about Palantir? I do.

In no particular order…

FastRadius. Cloud Manufacturing Platform - The Next Revolution in Manufacturing is here. From their latest Earning Report, they seem growing.

Tritium Charging. Creating the world’s most advanced and reliable DC fast chargers for electric vehicles. They just opened their first global EV fast charger manufacturing facility in the US. Business seems growing according to this ER. And it’s “just” 30% down from it’s listing price.

Celularity. Biotech company doing research on cell-based treatments focusing on T Cells, NK Cells via studying the placenta (fuck if I know, I’m no doctor). Unmet global need, groundbreaking research, pioneering technology. 150,000sq ft including laboratory and advanced manufacturing space for cellular medicine & bio-materials. Similar to the above, it’s ER report paint a pretty picture.

Rigetti Computing is an integrated systems company. We build quantum computers and the superconducting quantum processors that power them. Through our Quantum Cloud Services (QCS) platform, our machines can be integrated into any public, private or hybrid cloud.

What the actual fuck. Quantum computers are real. Ok let’s just pretend I knew that - I’ve heard vaguely something about IBM doing work in this, some brief mention of China doing some exploration but… yea ok. Let’s just… smile and wave.

BTW, remember the press angle I mentioned? Have a google for Rigetti Computing SPAC Palantir and you’ll see Reuters, TechCrunch, BusinessInsider, SiliconAngle, TheQuantumInsider, Nasdaq, Bloomberg, Capital.com, USNews and more (I got bored on the 2nd page) all covering this. TechCrunch at least prides itself on journalistic integrity so they don’t accept (to my knowledge) paid advertisement so what I’m trying to say - you can’t associate a dollar value to the amount of free press they’re getting just from associating with this sort of companies.Just last month they got awarded a DARPA contract for quantum application bench-marking. Their latest ER also seems promising - it talks about, uh, 84-qubit and 336-qubit systems.

Bird.co. Urban mobility start-up that sells electric bikes and electric “trotinete” - how do you call them in english? Scooters? I thought that’s something else.

They market them as scooters so… maybe foot-powered scooters? But they’re electric. What are scooters then if scooters which you use your feet to power ahead are also scooters like the ones you sit on your ass and honk-honk with like all those cool italian ones we see in movies? See, I vote we just use to Romanian “trotinete” and this particular ones are “trotinete electrice”- scooters are something else guys get up with the times.They allow people to start and operate their own fleet of electric trotinete using Bird’s software and hardware infrastructure. As of 04/09/2022 they’re currently down 95% (0.42$ stock price compared to it’s listing 8.40$ price) though that means they’re priced right now at 0.36 Price to Sales (market valuation RN is 106M$ and their revenue is 230M$). Their recent ER shows they got 103$ in a cash position so I’m guessing they’ll do just fine (I swear I got no clue though).

Energy Vault develops sustainable energy storage solutions that are transforming the world’s approach to utility-scale energy storage for grid resiliency.

Our proprietary Energy Management System software and Gravity-based Energy Storage Technology are intended to help utilities, independent power producers and large industrial energy users to significantly reduce levelized cost of energy while maintaining power reliability. Utilizing eco-friendly materials with the ability to integrate waste materials for beneficial re-use , Energy Vault is accelerating the shift to a circular economy and a fully renewable world.

This is in our climate-crazy media environment with all the “green-new-deal” type subsidies, WEF’s 2030

you will own nothing and you will be happyClimate Action Agenda, with exponentially rising energy costs (at least in Europe) and record profits for energy companies? Yeah I got no clue but they seem to be a fine investment. “Only” down 45% though with growing investments, a current valuation of $731M and growing revenues (they expect to bring in close to $700M by next year) I think they may be on to something if they manage to survive.Faraday Future. This is the one most bears seem to have their eyes set on highlighting. It received some DoJ attention regarding securities fraud, and are pre-revenue. Talks about it being an intricate scam similar to Nikola. They have some pretty pictures on their website of their newly made factory in California so, maybe? I dunno. In the latest ER, they say they’re expecting to start delivery by the end of this year, and as we know from TSLA’s “production hell”, starting a new auto plant is a highly capital-intensive feat. Down 90% so at a $300M market-cap, be it pre-revenue, I think if Palantir sees something cool with this, they can just outright buy it on the stock market (does it really work like that? Musk did with a chunk of Twitter though it might just have been for funsies).

Babylon Health. A company that provides health-care consultations through a mobile app. Seeing as how we view the US and the western-world as a pretty hypochondriac-prone nation, I can see the appeal. Down 93% so at a current market cap of $286M. It 4x’d it’s revenue on 2021 according to this ER, and according to the latest August Q2 it’s on track for $1BLN revenue for FY 2022. Actually now that I think of it, the question shouldn’t be why Palantir invested in these companies at frothy-valuations, it should be why doesn’t Palantir double down and gobble them up on pennies on the dollar compared to just last year, when they’ve had a bit of time to see how they work?

We develop transformative medicines and technologies by building agile, focused companies called Vants.

I’d just invest based on the heterobifunctional degrader thingy they mention on the website - a heterobifunctional degrader sounds hilarious. Okay jokes aside they seem to have all sorts of new medicine on the pipeline (Dermavant, Priovant, Immunovant, Femavant, Kinevant) and with a cash position of $2 billion from their latest Earnings Report, even though it still has tiny revenues ($4.3M if I understand correctly), I’m thinking it’s a cool bet from Palantir. They have their fingers in the pie with their healthcare platform thingy, the FDA and NHS partnerships so this seems right in line along with the other bets in the healthcare industry.

Blacksky. Real-time geospatial intelligence with a proprietary AI SaaS and terrestrial sensor network. Due to PLTR’s hush-hush work with the government this sounds nice. Also, I read somewhere on seeking alpha that some lady got a call from her nephew that works in “high-places” in the UN IIRC telling her to dump PLTR because ESRI does what PLTR does (lol) and is getting more attention. To that note, Blacksky and ESRI just launched a partnership, so I think they’re more friendly than it appears. Down 80% as of today, they’re starting to draw in revenue - and they have a new sales position advertised on their website solely responsible for selling to the DoD.

AdTheorent. ML and data-science solutions for advertisers and marketers that advertises some cookie-less solutions (nice with apple’s privacy changes). Q2 revenue according to the ER is up at $42.5M so I guess they may be on to something. Marketcap at $228M, down 74% from launch.

Boxed. Wholesale retailer - so this is an odd one if you ask me; I mean - going up against Amazon or Costco - but without the membership fees? Takes some balls. According to their first ER after going public, they say the’re licensing it’s end-to-end e-commerce platform as a SaaS plus homegrown automation robotics for fulfillment. I dunno what robotics mean in this instance but my eyebrow’s raised on the intrigue. With 2021 revenue in at $177M they’re still burning cash from what I can tell (supermarket margins being crazy small) though from it’s dwindling marketcap ($70M, -90% down) I’d vote that palantir just buys it with it’s spare cash from between the couch’s cushions should they fancy.

Lilium. The first electric vertical take-off and landing jet. I dunno what it’s good for yet but it sure looks fancy. Their 2022 Q3 ER says nice things though since it’s pre-revenue, burning cash and just ramping up testing and production this is a true wild card. Could go tits up or not. The pretty pictures with all those engineers in a factory sure seem reassuring though. Marketcap’s at $652M though after a 77% dive after IPO - could go down way more. Or up - who am I to say. I hope they survive though, I always wanted to live in the future, and this is as close to the Jetson’s era as we’re gonna be. Just imagine commuting to work with this.

Pear Therapeutics. At the intersection of software and therapeutics, where researchers work with developers for next-gen software based therapeutics. I still don’t get what that means but I’ll play along. They posted $3.3M revenue in the latest Q2 2022 ER, so someone’s giving them money. Seems in-line with Palantir’s healthcare ventures.

Wejo. The world’s largest source of connected vehicle data, unlocking the data in autonomous, connected and electric vehicles. The CEO’s hosting AMA’s on his reddit account so that may be fun to read. They posted $2.6M revenue for 2021 but it’s a drop in the bucket compared to their net losses ($218M) so who knows if they’ll make it? Pretty website though! It mentions quite a few use cases and do mention the word platform in there’s that.

Sarcos. Robotic avatar-suits for humans (they said it not me). Started beta-testing. Burning cash like crazy.

Astrocast. Satellite IoT provider for all sorts of industries. According to MarketWatch, their market cap is 375M NOK so that’s $37.5M if I’m reading this right. Pre-revenue though they’ve been successfully launching satellites and acquiring companies. Didn’t bother to click on their ER reports but this sounds fancy.

FinAccel. Some sort of loan company in Indonesia? I got no clue what to write about this.

So with all these companies’ valuation cratering I wonder if Palantir outright buys ‘em and takes them in-house as off-shoots to showcase it’s powers. You know how in texas hold’em you gotta pay a blind just to be able to see the cards? I think of this play in the same way - maybe now that they see the cards of each company, one might prove to be a decent acquisition and let do it’s own thing. Tough to say now as most are still risky so I guess it’s good they don’t have me in charge of those decisions.

Actually - I’m sort of hoping they do end up purchasing a couple of companies. I’m actually pretty sad that they’ve discontinued the SPAC programme for this year, I’m fond of this strategy. I get to sit on my couch and watch the company make reasonable bets with all the cash they got laying around?

3.2 Palantir for Builders

With this they provide their platform for start-ups also in crazy industries that no one would have thought possible just a few short years ago (KatalystDI people have said as much in the interview). What I can’t tell here is the $ amount they’re getting for their services - I imagine it ain’t free (their other clients wouldn’t be happy about that) so we guess it’s a confidential sum or arrangement - maybe they have some equity promises or convertible notes involved?

I think they’re angling for proof of concept in all these juicy industries so that they can then sell even better customized solutions to the big guys.

Anyway, so far they’ve announced 12 partnerships in the following industries: blockchain analytics, construction supply chain, an AI company focused on optimizing wind farms, a company that enables consumers to take control of their own browsing data, an australian-listed drug development and clinical care company, European Cricket Network (check out the reddit - mad engagement), a healthy food buying company, an industrial robotics company, fintech buy-now-pay-later solution, a UK-based AI company for the legal and consulting industries, one that helps customers understand Medicare plans and a company focused on tools for the distributed workforce. Read all about them here and here.

Entire new industries are battle tested and built upon Foundry.

3.3 Developer network

This year Palantir started it’s '“For Developers” network. YouTubers have gone to great length to explain why that’s awesome but as an investor I see this similar to how SAP and Salesforce have certification programmes. Both have spawned an entire ecosystem of industries tailored to them. I think of it in the same way as the iOS ecosystem - apple provided the tools and then people went on building all sorts of cool stuff with it. While I couldn’t have fathomed the gigantic reach of how Apple’s app ecosystem evolved when I first saw an iPhone, I even ended up developing apps through my dev company so to allow people in the 3rd world earn a living independently of the company is one key aspects that reflects how entrenched companies like apple have become in our daily lives. While there’s no guarantees, I feel the same way as I’m watching the seeds of a similar approach being planted by Palantir.

You can read all about it on the website and through CodeStrap’s YouTube technical dives into the platform. I think it’s also wise that they’re offering the platform to the hands of select ambassadors.

3.4 Partnerships

So bears like to say that “it’d take google or microsoft or AWS just a bit to copy Foundry and compete”. Sure, I guess that’s the innovator’s dilemma - that’s why we had MySpace before FaceBook.

To that - I’m pretty confident they aren’t pursuing developing a competing solution, rather the big guys are partnering with Palantir. Like Google, AWS, Carahsoft, Accenture and IBM.

One partnership I couldn’t figure out if it’s part of the For Builders programme or if it’s an equity investment or whatever is the one with Rubicon - a company that provides solutions for the global waste problem. You can read the hilariously titled “Palantir is Getting into Garbage in Partnership with Rubicon” on their website.

Beyond that, they have a new partnership announced with Better (digital home- ownership platform) and Beckett Collectibles though I got no clue how it works on the back-end.

4.0 It’s sales strategy, current and potential valuation, bear case and risks

4.1 Sales strategy

The guys over at FourWeekMba do a pretty good job of explaining the acquire, expand, scale model. Rather than re-iterate those points, I think I may add some context.

So in their latest Q2 ER which the market envisioned as disastrous (I liked what I saw) they posted a customer increase to 309 customers, up from 169 just last year - up from almost 100 that they’ve had at their DPO (just 1-2 years after they launched Foundry commercially). So they make most of their money after the 3 year mark of their engagements. So there’s 100 new customers that will be reaching that stage the next two years. And if they keep this up, there’ll be a steady stream of customers that reach that stage each year.

Now I’m not a numbers guy but that seems like a 100 snowballs turning into 100 avalanches.

With their constant 80% gross profit and sticky business model, coupled with the fact that they’re driving their costs of implementation down consistently I think this’ll print and scale similar to how software companies operate - after all, once the implementation’s done, why would you keep sending a team to implement again? It’s just maintenance work, which could be done theoretically by people inside palantir that are not that high up the chain.

I just fail to see how people say that because they’re sending people in for the implementation phase that this is similar to a consultancy. I mean - have they not seen the videos with the actual software? It’s… software. Yes, supported by people because each company is it’s own unique ball of clusterfucks. But you don’t implement it again year after year; you maintain it. Yes it’s not pure software margins like DocuSign or whatever but this is one complex beast that needs custom work to tailor. But after said tailoring is made? Sure, the customer can gain weight or whatever analogy would fit, but most of the tailoring is made.

So they specified that their TAM is $120BLN, judging from 6k companies world-wide that are in countries that they’ll do business with.

I think that’s a conservative estimate.

So as the global economy gets bigger, it’s safe to say companies will make more money - and new companies will be on the list of potential prospects. There’s this top 2000 worldwide companies in this forbes article that, sure - includes Russian and Chinese companies (that’s a no-no) that all have revenues over $2,5BLN. I have no conclusive research on this though I’d guess there are more companies that do higher than $500M/year revenue than 6000 worldwide. But what about India, Africa and South America? I think there’s growth in lots of places that will take off. Also, there’s this 2015 list of top 1000 companies in Romania. Sure, not a lot of contenders - but I just picked a company at random - Ardealul SA that brings in $100M in revenue. That’s far from their stated $500M revenues and over, but they’ve grown to $100M in revenue from $16M in 2005. And this company deals in corn - nothing too wild. Their website looks like this.

My point? If I’m looking at the local market and how we’ve learnt to deal with all this capitalism, there’s lots of others around that are getting the hang of it - and their growth far outpaces our own. So, to me, it’s a safe bet that as the world economy grows, so does the potential market of Palantir.

4.2 Their sales team

So for the first 10-15 years or so they only had Karp handling sales personally. It made sense considering their focus on US government. Now they’re targeting commercial accounts globally and they’ve just started hiring a sales team.

They on-boarded 80 sales people by the end of 2021 (check it out in FY 2021 Business Update) out of which just 25 had tenure over 9 months.

They ended 2020 with 12 sales people - out of which just 6 had tenure over 9 months (which they consider the minimum length one gets accustomed to it’s products). So there were six sales people up until 2021’s first quarter. Six. And they still managed to land close to 200 customers since it’s DPO in september 2020 - 40 of which in Q1 2022, 27 is Q2. So these 67 from the first half of 2022 will enter the scale phase by 2025. Yeah, 67 snowballs just this first half of a year.

And consider that tenure doesn’t mean instant results. Sales cycles in B2B software are long. I mean even 18 months long, depending on who you listen to. Considering such a complex software, I think even longer.

You gotta remember it’s not b2c - like tesla for example, where it’s products are out in the street and people can fawn over and recommend to their friends. Since PLTR brings competitive advantage, companies tend to keep quiet about that - hence the reliance on a sales team. Sausage companies don’t want other sausage companies to know how they make better sausages faster and cheaper. I’m actually surprised we’ve been able to see the actual names of the client companies.

This year they got in Philippe Mathieu as president of Palantir EMEA. This guy is a software OG having brought in ¬$16BLN for Oracle. Also, judging from their career page, they’re still expanding their sales-force. Middle of a recession, when lots of other tech companies and otherwise are firing people.

Extra juicy? They’re developing offices across the world. From their contact page, they have offices in Copenhagen, Paris, Munich, Tel Aviv, Amsterdam, Oslo, Stockholm, Zurich, Abu Dhabi, Ottawa, Canberra, Sydney, Tokyo and London (in addition to their 5 USA offices). Pretty rich countries (14 I think).

Since I’ve read somewhere on the internet that their average revenue per customer is $5.6M / year, they’d need to on-board close to 900 clients by 2025 in order to produce $5BLN / year by 2027. Ambitious? Sure - but doable, I think, with 300 already signed up.

Also, I’ve only been thinking about Foundry or Gotham. We don’t know how Apollo’s pricing works or how their different platforms (MetaConstellation, HyperAuto, Skywise, the one for financial services, PLTR for crypto, etc.) work - and neither their potential market.

As well, I’m not one to speculate though from the R&D costs I don’t think they’ll stop at producing other products. I’ve read other people think they gotta go B2C in order to reach a marketplace in the trillions though I feel that’s a bit too minority-report for my style - I prefer to deal in a more immediate possible future based information we have available so far. Though, like I mentioned before - 10 years ago we barely had mobile phones.

Actually, I have a friend here that owns a bar. Pretty blue-collared mindset but like everyone else he has gadgets, a PS4, whatever. He asked me about bitcoin a few years ago and we’ve ended up talking a bit about tech. And he said something that I think’s pretty smart - if 10 years ago you would have seen someone on the street talking to himself, you’d have thought he was crazy. Nowadays with blue-tooth earphones, not so much. So - who knows? Maybe we will have a sort of siri / palantir hybrid that we can ask to plan our calories for the day or make the best cost-effective travel suggestions. Maybe through a different SPAC or for builders initiative.

4.3 Current and potential valuation

As of today, it’s trading at $7.40 for a $15.4BLN market cap. As it’s valuation plummeted due to QT reversal (which - I have no clue what the future will bring in this regards; I’ve only been in the markets post 2008 when Americans we’re pumping money) it may very well continue it’s downward trend.

From what I can get, this is macro driven; seeing as how all growth stocks have plummeted as investors went in search of safe-haven value stocks. I figured it may pay off to stay invested as there’s no point in chasing trends and if the stock is getting cheaper while the business is growing it’s an opportunity to DCA. While I got no clue what the bottom will be, I’ll be happy to nibble my way downwards and upwards. I’m pretty sure the americans will start the money printer sometime again (is there any other option for them at this point?) so since this is a company directly connected to the tit of the money printer, I feel I should be fine.

I’ve known of the lock-up period and figured I’d keep a % to average down - thought that paying a premium would make sense; if it went down I thought it’d be fine as that’d be an even better entry point. I watched it climb up to $45 (still didn’t sell all of my position - was aiming for $60 at the minimum regardless of how long it took) based mostly on pre-lock-up period hype and retail investors.

Seeing as how there are tons of eyes on this judging from the amount of coverage this gets and how they’d need one big contract from daddy government for the stock to jump, thought it’s worth the risk premium (considering at the time rising geopolitical tensions which are now starting to manifest). That $800M deal with the US Army served as further confirmation.

Remember my earlier point that there are millions of retail traders in our connected world? This just wasn’t possible previously. Now people all over the world are looking at stocks. As it’s valuation gets lower, this is making it’s way into value stock territory, which is bound to attract a different breed of investor - the one that buys stocks as partial ownership in the company rather than looking to trade.

How I have a theory that capitalists love crashing their economy so that they can buy assets on the cheap every few years, I’m thinking that I’ll just keep on to my shares through the waves of economic cycles. Right now, retail owns 60% of Palantir. If more institutions want in, they’ll have to buy them from us plebs. So, yeah - why would I sell now?

As we’re entering into a what I feel is a manufactured crisis, I’ll be doing what the capitalists plan on doing - buy assets in companies I want to keep for the coming decade. I think their plan is on us selling stock at really depressed prices so we have what to buy food and gas with. Yeah, no thanks - hope it doesn’t come to that but as with investments one needn’t rely on money in the stock market with a short time period.

They’ve told us that the semiconductor shortage was due to corona (as if there are little asian people in factories hand-making chips rather than big ass machines), after that - supply chain issues because corona (trucks and cargo ships seem to me as fairly safe bets one would have himself be in the midst of a pandemic), after that rising energy prices (because, of course, corona), exploding raw material prices (you betcha - corona) and that’s across the globe (even in Eastern Europe us plebs gotta pay big energy bills because somehow corona and now the latest pretext is because Putin). The coming winter is poised to be brutal, what with Germany and UK and other such countries’ energy prices going through the roof. Even locally - demand for wood-powered stoves has shot up. As has in Denmark or Austria.

What we’ve initially seen in 2008 in our corner of the world was the Dacia plant (car manufacturer) placing it’s workers on a part-time basis, and then, layoffs. Due to the rising costs of energy, we’re starting to see similar issues - local factories that are handling fertilizer production, aluminum and other chemicals are experiencing problems due to the supply chain. Interesting that fertilizer’s one of the first to experience problems, what with the Dutch people’s plight with their government wanting to ban nitrogen-based fertilizer, Trudeau having recently jumped on that bandwagon too (wonder where he got the idea). Also Polish fertilizer factories are experiencing hardship due to increasing gas prices. Likely more - haven’t paid attention in detail to this.

So the writing’s on the wall - whatever comes, won’t be pretty for a lot of us. This time around the signs are being felt simultaneously on a global scale. Capitalists’ and globalists’ alike wet dream though.

To tie this back in to Palantir, as it’s valuation plummets, counterintuitively it’s inherently less risky to invest even for us plebs. Seeing as how I’m certain there are lots of funds out there that don’t even look at stocks with a less than 5 year public trading history, there’s money to be made for us gamblers. For the rest of us that got a bit trigger happy - well, I’ll just stick to my plan and chip away. Hopefully by the time Americans warm up the ol’ money printer or start throwing money to AI in order to one-up China I’ll have loaded up on cheap shares.

Speaking of - remember that the White House approved a big spending bill towards AI? On the FY report from the AI.gov page, we can read in the intro about something they call “Digital Twin Earth”. Now, where have we heard this phrase before? Anyway, the bill is for billions of $. Even if this doesn’t flow directly to Palantir, the companies that will be benefiting I guess will end up running it’s business on Foundry. Rising tide raises all ships. Also, the current Director of National Intelligence is ex-Palantir. Couple that with the $50BLN Chips act and this environment looks promising for our AI overlords.

Back to our current valuation and how the internet rages that this company’s bad to it’s shareholders. Look, it’s not our god-given right to invest in the CIA’s business. And if you’ve done your research, you’d have known that management has controlling interest regardless of the amount of stock they sell (bye bye SP500 inclusion in case anyone was wondering). They don’t have to answer to share-holders. Yes, horrible, I know - I personally like it that way.

If it were up to the screeches in seeking alpha’s commentary section or on Palantir’s For developers channels where they have allowed commentaries we’d have a vastly different company.

And sure - they could, in theory, “return value” to shareholders - if they cared about that in the short term. They could fire half of it’s staff and ride on a skeleton crew all while servicing it’s current $3.5BLN in remaining deal value and raise it’s current EPS exponentially. That’d get rid of that pesky SBC we keep hearing about and turn this into a short term Wall Street darling. Hell, they could even issue *gasp* dividends then! BUYBACKS!

I view them not having to answer to shareholders as a net plus. Imagine if they’d have a board to answer to - ran by greedy wall-street types that care about QoQ numbers. As we’ve seen from the sort of questions people have asked of them in the earnings call, suffice to say, retail people aren’t the brightest of the bunch. As Ford said - if you’ve asked people what sort of transportation they want, they’d have said faster horses.

To that note - they are already profitable - just not on a GAAP basis. Just look at their growing FCF and cash on hand without debt. I dunno how taxes work in the US but over here if you post profits, you also pay tax. I’m fine with legal tax evasion if it means reinvesting into the company - just take a look at how Amazon has done things; it took Amazon 14 years to post profits (by 2017) - when it’d already been entrenched in the global economy. By comparison, yes, PLTR is launched 17 years ago, but it’s been researching in the shadows, perfecting it’s product for government clients on government dime, with no ambition so far of expanding globally. In the first 14 years or so, they only had Karp handling sales.

So instead of returning immediate share-holder value, they’ve expanded their salesforce globally and developed partnerships with all those cool companies that will in turn offer the product to their existing relationships. They’ve been building products and ran on a massive 30% hiring spree since the DPO that’s still going on. They’ve developed their footing in all the rich countries. Expanding their sales team, which will fully ramp-up in a few years time, will draw in clients that will start printing by the 3rd year or so of their engagement. Like Karp said - if you’re looking for immediate value, there are lots of other stocks.

So in regards to future valuation, we have the guy from Daily Palantir do a YouTube video with an analyst with his own neat little juicy confirmation-bias-producing pretty excel file (here’s the link from the YouTube description to the valuation if you want to play with it). I don’t place much faith into excel files - I’m here based on the company’s goals of producing best in class software, developing platforms that will support the future’s industries, it’s virtually 0 competition. I’m thinking that should they accomplish what they set out, it’s valuation will likely reflect that. My original goal was to get out at $60 or re-evaluate by 2027. Maybe it’s blind faith or an educated guess - time will tell I guess.

As for SBC and management rewarding themselves handsomely - Karp made close to a clear billion from what I can gather due to his stock options. That’s after 17 years with the company (he even had dark hair when he got on-board). Don’t know about you but I’m fine with the people in charge raking it in. It’s their company, lol. And he could have called it quits and retired on a beach somewhere but no - still on the front-line. I personally wouldn’t trade my life with Karp’s, regardless of monetary value. I like my freedom - he has to walk around with private security. So now it’s less about the money for him - he’s in it for the vision. Also, they’ve awarded themselves said options 10 years ago - when they had no clue if they would be going public ever or if they were on to something big. It’s not like he wakes up in the morning, checks the stock price, and hits sell on the way to the office. They announce this sort of things in advance otherwise the SEC’d be all over them.

Back to it’s valuation, we have some press (VanityFair is one I could find without a paywall) saying Morgan Stanley we’re thinking of taking this public at a $41BLN valuation through an IPO. They ended up taking a DPO that came with an $800M price associated with - in part, to say F wall street and, in part, due to Karp’s socialistic tendencies I think. It’d have dumped likely just as hard should they went that route post QE and divind head-first into QT but this way us little guys have a fighting chance to build up a position IMO. One thing we have going for us is time and patience.

4.4 Bear case and risks

I’ve tried long and hard about potential thesis breakers. So far, only one I’ve identified is the risk of being hacked. That, I think, would instantly collapse it’s share price.

I think it’s moat is too wide for other contenders looking to emulate their success - they’ve invested for close to two decades now in shaping up the platform with some of the brightest minds there are. Even if say Google or Microsoft was looking to compete, they have quite the road-map ahead of them just to catch up - even if they have a solid picture of what that’d look like, they can’t just CTRL-C / CTRL-V the source-code. Palantir owns it’s fair share of patents, which sure can be worked around but would prove to be tricky.

A bear case scenario would be that companies are less likely to spend coming into a recession, so growth would slow down - which is to be expected though I imagine Palantir’s promise of providing competitive advantage to negate this. Even if they manage 0 growth while the economy’s looking back up, their sizeable cash position and remaining deal value (close to $6BLN combined) should help them fare pretty well.

Another bear case for investors would be further diluting the stock faster than they can offset in revenues and / or profitability. That to me is also fine - I’d rather they keep cash on hand and make this company recession-proof and maybe do some cool acquisitions along the way while they retain top talent with stock options. Besides, it’s not like they hand out SBC like candy - there are contracts for them; as they typically vest over a 4 year period.

5.0 It’s raving fan base

So on their /PLTR subreddit we have close to 50k subscribers that are pretty surely in it for the long haul. Beyond that, I’d guess there’s a way higher number of lurkers that don’t bother joining or contributing to the reddit. Though from threads like this one, it’s base seems knowledgeable and loyal.

Also, there’s this guy Magikarp_to_Gyarados I’d like to single out due to his participation in the forums. He’s done an amazing, thankless job of clearing FUD regarding the stock. I’ve read I think all of his comments as they’re particularly insightful as he goes deep into the company’s documents to provide rebuttals to most of the aspects one could have regarding this company.

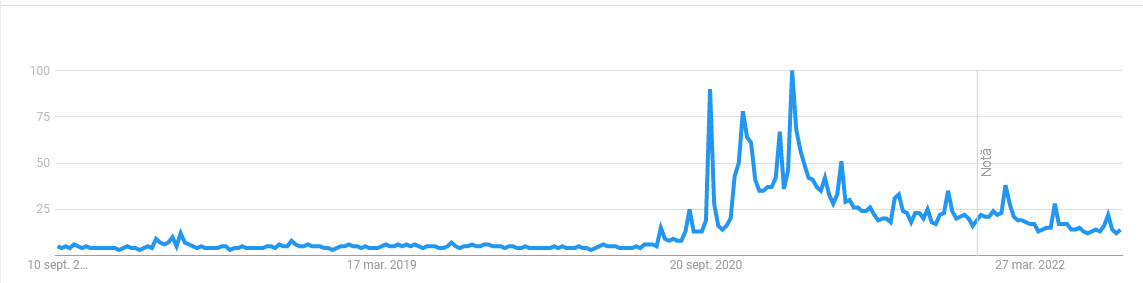

Beyond that - we have all the youtubers that have been providing coverage, and the incessant SeekingAlpha coverage. Bears and bulls alike, they’re sure to get eyeballs to this. And remember the previous screen-shot showcasing close to 400k google searches / month on various PLTR related queries? This, to me, is a massive indicator as to this stock’s popularity.

So let’s say as a thought experiment that the 50k /PLTR subscribers own on average 2k PLTR stocks. That’s close to 100M of stocks that are pretty likely to HODL.

As well, as the guy running Daily Palantir points out - there’s this genius mathematician that owns 28M PLTR stocks through his Renaissance Fund, up from December ‘21 when he had 15M.

Stanley Druckenmiller, one of the world’s legendary stock pickers, also owns Palantir to the tune of 4.2M shares.

As far as I can tell, Vanguard or Blackrock own close to 10% of the stock so far - I think it’s a forever type of holding for them. As they own a bit of everything this is not saying much but it’s 10% of the stock that likely won’t be traded anytime soon.

Canada’s Pension Plan still owns 7M shares. From the word Pension in the name, I guess it’s also a long play.

Snowballs to avalanches - eventually, people who want in, will buy in from retail. Who else from? We own 60% of this. Insiders own 6.5%, and I doubt institutions are looking to sell anytime soon - especially these days, seeing as how it’s trading lower than it’s DPO price. This places most investors underwater - and will likely draw it’s own crowd just for that aspect.

Currently, Fintel reports 32% institutional holding, which is slowly increasing each day. So demand’s building up, press is continuing to talk about PLTR, google searches are up - those are pretty positive sentiment indicators to me. Check out the google trends analysis for bitcoin - it overlaps almost perfectly to it’s price surges to 20k and then 60k, and now back. My guess is that’ll happen to Palantir too.

There are millions of traders and investors world-wide, with access to information and most recently - access to low or no fees stock trading. The stock market having previously been a tool for the already-rich, we’re in uncharted waters regarding retail interest. I’d guess most retail investors are up to 35 years old - and there are millions more attracted to the game each year (world population’s growing along with access to technology in countries that barely had electricity few years ago).

All of us having witnessed BTC, TSLA, GME, AMC and most recently BBNY we can all safely say that retail can move markets. As does this wharton study points out and this BNY Mellon study.

I’m pretty certain there are lots of us that have rolled TSLA → PLTR, even more of us that come with a “background” in crypto and a quick in-n-out with GME.

I think this checks all the hallmarks for retail trader / investor interest. Meme potential? By the truckloads - Karp’s hair and it’s inherent memeability from it’s name and association with LotR. Blindly loyal fan-base? Yes - they’re hilarious.

In closing, I’d like to mention a recent idea I learned from the internet.

Volatility is the price you pay for returns.

Volatility ≠ risk.

YOLO?

YOLO.

6.0 Additional copium & reading material

This SA coverage regarding Alex Karp’s talk at the World Economic Forum provides an idea that PLTR is essential to the US’s military dominance. The idea is that since US has 700 bases world-wide to keep track of, PLTR is suited to provide better resource management. I think that could be extrapolated to commercial clients. Second one being that PLTR’s value is always 5 years away from being understood. This other SA article ties into my previous idea that just by being 80% off it’s highs will atract it’s own crowd that weren’t previously interested in what could arguably be construed as outrageous multiples (I still think that a company like this deserves a high multiple - though I have been ‘brought up’ on the idea that growth stocks earn a premium of 40x sales, ballparking. I may have gotten this idea from forums - I’m no specialist. Even so, I found the premium be worth it in case the company signs some surprise billion dollar contract - confirmation bias from that US army deal).

CodeStrap’s channel is interesting for those that want to better understand the technical aspects of the company. He’s a Foundry ambassador with access to the platform.

I’ve wanted to provide some links that better explain how Palantir’s Apollo works though I haven’t found any that can ELI5 this to me.

Arny Trezzi’s substack provides some interesting insights.

As does Antonio Linares’ substack.

Referencing this again for good health - it’s a good read: https://insights.greyb.com/palantir-patents/